Many retail traders assume that “instant funding” is just a faster version of the standard prop firm challenge. It isn’t. The distinction matters more than most people realize, especially if you’re preparing to enter a proprietary trading program and need capital access without waiting weeks for evaluation results. Instant funding accounts operate on a fundamentally different model, one that skips the demo phase entirely and puts real capital in your hands almost immediately after payment. This guide breaks down exactly how these accounts work, who they serve best, and what you need to watch out for before committing.

Table of Contents

- What is an instant funding account?

- How do instant funding accounts work for retail traders?

- Comparison: Instant funding accounts vs. traditional challenge accounts

- Major benefits and common pitfalls of instant funding accounts

- A critical perspective: Who should (and shouldn’t) use instant funding accounts?

- Next steps: Choose the right instant funding option for your trading future

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Immediate access to capital | Instant funding accounts let you trade with firm capital right away without passing an evaluation. |

| Strict rules still apply | Even with instant access, profit targets and drawdown limits are enforced by most firms. |

| Speed vs. cost trade-off | You pay a premium for skipping challenges, so weigh higher fees against time saved. |

| Best for experienced traders | Instant funding accounts are ideal for traders who are confident in their skills and risk controls. |

What is an instant funding account?

An instant funding account is a prop firm offering that gives traders direct access to live trading capital without requiring them to pass an evaluation or challenge phase first. As noted in our review, instant funding accounts offer access to trading capital with no evaluation phase. That’s the core distinction from traditional models, and it changes the entire experience.

With a standard funded account, you typically go through one or more stages of assessment. You trade on a demo account, hit a profit target, stay within drawdown limits, and only then receive access to real capital. This process can take weeks or even months. Instant funding removes that barrier entirely.

Here’s what you typically get with an instant funding account:

- No demo or evaluation phase before accessing live markets

- Real capital allocated immediately after purchase and account setup

- Direct market access from day one, across forex, indices, or commodities depending on the firm

- Profit split arrangements that begin as soon as you generate returns

- Risk parameters in place, including daily and overall drawdown limits

The traders who benefit most from this model are those who already have a tested strategy and consistent discipline. Speed is the primary value proposition. If you know how to manage risk and want to start generating returns without the friction of an evaluation, instant funding is worth exploring. You can also compare instant funding vs evaluation programs to understand which path fits your current skill level.

Pro Tip: Instant access to capital does not mean fewer rules. Most instant funding accounts still enforce strict drawdown limits and trading conditions. Read the terms carefully before you pay.

How do instant funding accounts work for retail traders?

With a basic definition in hand, here’s how the process typically looks for retail traders who want to get started.

- Choose a firm and account size. You select a prop firm offering instant funding and pick a capital tier, such as $10,000, $25,000, or $100,000.

- Complete the application and pay the fee. Unlike challenge accounts where you pay to attempt an evaluation, here you pay for immediate capital access. Traders receive real capital after payment, not after passing a test.

- Receive your account credentials. Within hours, you get login details for a live trading account funded with the agreed capital amount.

- Start trading immediately. You can place trades in real markets from day one, subject to the firm’s risk rules.

- Request profit withdrawals. Once you’ve met the minimum trading period or profit threshold, you submit a payout request.

Most instant accounts allow withdrawals within 7 to 14 days after the initial trading period. Payout splits typically range from 70% to 90% in the trader’s favor, depending on the firm and account tier.

There are restrictions you need to understand before you start. Every instant funding account comes with a maximum daily drawdown (often 4% to 5%) and an overall drawdown limit (commonly 8% to 10%). Breaching either limit results in account termination. Some firms also restrict trading during major news events or require minimum trading days before a payout is processed.

“The appeal of instant funding is real, but so are the conditions. Traders who skip reading the fine print often find themselves disqualified within the first week.”

Understanding how these programs differ from broker accounts is also useful. Our breakdown of programs vs brokers clarifies where prop firms end and traditional brokerage begins, which affects everything from leverage to liability.

Comparison: Instant funding accounts vs. traditional challenge accounts

To make the benefits and drawbacks clearer, let’s put instant funding side-by-side with the traditional challenge route.

Standard challenge-based accounts require passing a multi-stage evaluation, often with profit targets and drawdown constraints. That process filters out undisciplined traders, but it also delays capital access significantly.

| Feature | Instant funding account | Traditional challenge account |

|---|---|---|

| Time to live capital | Hours to 1 day | 2 to 8 weeks |

| Evaluation required | No | Yes (1 to 2 stages) |

| Upfront cost | Higher | Lower to moderate |

| Profit target to qualify | None | Yes (typically 8% to 10%) |

| Drawdown rules | Yes | Yes |

| Profit split | 70% to 90% | 75% to 90% |

| Best for | Experienced traders | Developing traders |

Instant funding accounts: pros and cons

- Pro: No waiting period before trading real capital

- Pro: No risk of failing an evaluation and losing your fee

- Pro: Immediate feedback on real market performance

- Con: Higher upfront costs compared to challenge fees

- Con: Strict risk rules with no buffer period to adjust

- Con: Less room for error in the early days

Traditional challenge accounts: pros and cons

- Pro: Lower entry cost in most cases

- Pro: Evaluation phase helps build discipline before going live

- Con: Time-consuming, especially with multi-stage programs

- Con: Risk of failing and repaying to retry

The right choice depends on your experience level and goals. If you’re still developing your strategy, the evaluation process in a challenge account can actually protect you from blowing a live account too quickly. Reviewing funded trading strategies that work in live environments can help you gauge whether you’re ready for the instant route.

Major benefits and common pitfalls of instant funding accounts

Understanding the pros and cons upfront can make or break your success. Here’s what to keep in mind before you fund an account.

Key benefits:

- Speed: You skip weeks of evaluation and access capital within 24 hours

- Simplicity: No multi-stage challenge structure to navigate

- Real market exposure: You trade live from day one, which builds genuine experience faster

- Profit potential: High payout splits mean a larger share of your returns stays with you

Common pitfalls:

- Hidden fees: Some firms charge scaling fees, inactivity fees, or platform fees not listed prominently

- Tight drawdown rules: With no evaluation buffer, a few bad trades early on can end your account

- Profit split fine print: Some firms reduce your split if you don’t meet certain consistency rules

- Withdrawal delays: Not every firm honors the 7 to 14 day window they advertise

As our analysis confirms, not all instant funding accounts are created equal. Traders need to review terms closely before committing. This is especially true for withdrawal policies and risk management conditions, which vary widely across firms.

Most frequent mistakes new users make:

- Choosing a firm based on price alone without checking payout history

- Ignoring the daily drawdown limit until it’s too late

- Failing to track minimum trading day requirements before requesting a payout

- Not verifying whether the firm is independently reviewed or rated

Pro Tip: Before signing up, check independent sources like Trustpilot and trader communities on Reddit or Discord. Cross-referencing payout data from real users gives you a more accurate picture than any firm’s marketing page.

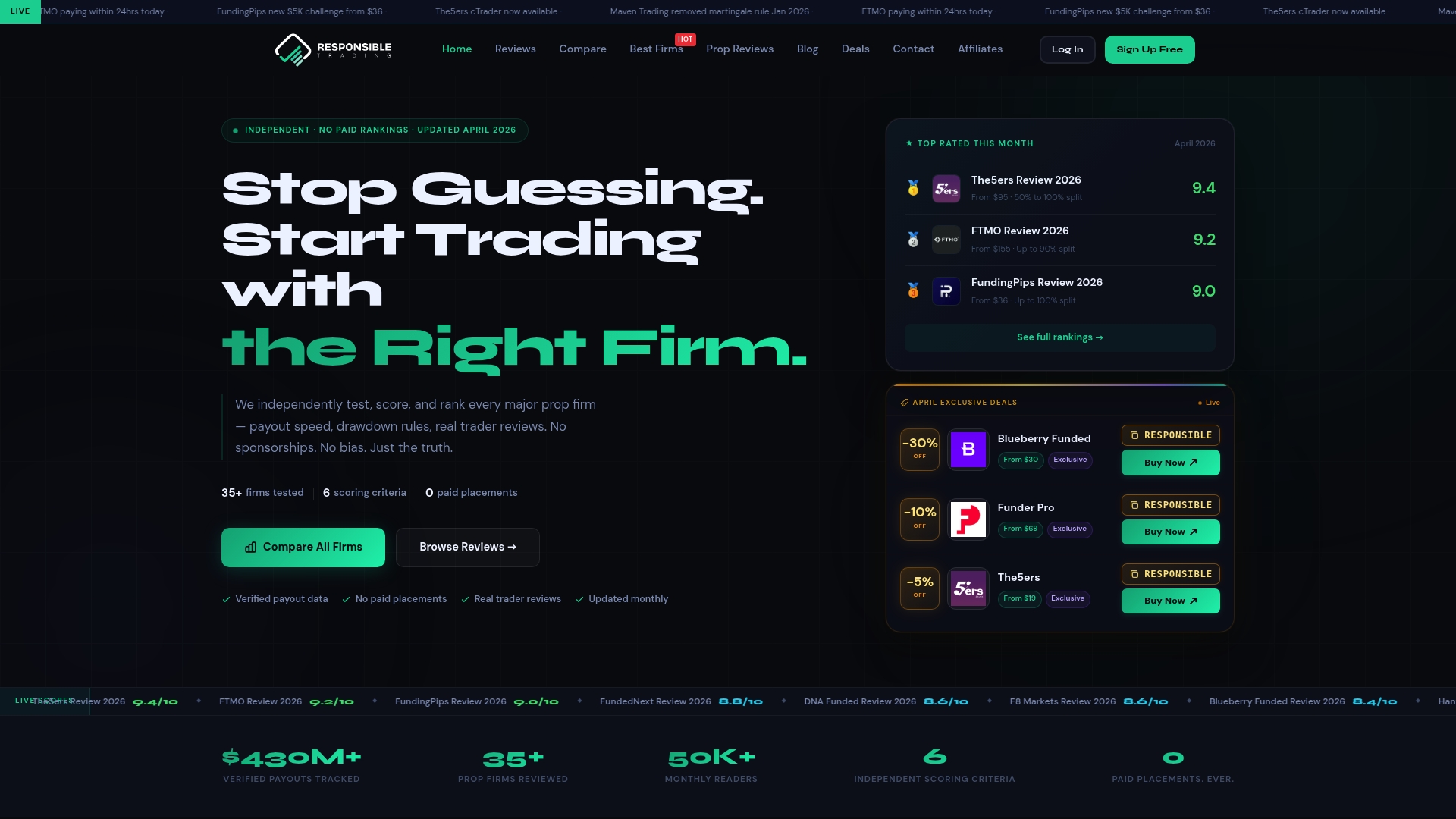

For a curated list of vetted options, our best prop firm rankings provides objective scoring across payout reliability, rule fairness, and overall value.

A critical perspective: Who should (and shouldn’t) use instant funding accounts?

Having covered the nuts and bolts, let’s take a step back for some candid advice.

Instant funding is not the “easy mode” some traders expect it to be. The absence of an evaluation doesn’t mean the firm is lenient. In many cases, the opposite is true. Because there’s no assessment phase, firms compensate by applying tighter risk controls from the moment you start trading. One or two volatile sessions can end an account that cost significantly more than a standard challenge fee.

Experienced traders with proven discipline and a consistent edge are the ones who benefit most. They don’t need the evaluation phase to validate their strategy because they already have data from their own trading history. For them, instant funding is a genuine shortcut to scaling capital.

Beginners and traders still refining their approach should be cautious. The speed of access works against you if your risk management isn’t solid. Losing an instant funding account is more expensive than failing a challenge, and it doesn’t come with the same learning structure.

Our in-depth prop firm reviews consistently show that responsible trading means matching opportunity with personal readiness, not just responding to appealing offers. Due diligence always beats speed when real capital is on the line.

Next steps: Choose the right instant funding option for your trading future

If you’re ready to take action, here’s where your research continues.

Choosing the right prop firm is as important as choosing the right account type. Not every firm offering instant funding delivers on its promises, and the differences in payout speed, drawdown rules, and profit splits are significant enough to affect your bottom line directly.

ResponsibleTrading.com provides independent, data-backed reviews and comparison tools built specifically for traders evaluating prop firm options. Whether you’re looking for the best forex trading platform or want to compare prop firm challenges side by side, our tools give you the objective information you need to make a confident, informed decision before committing any capital.

Frequently asked questions

Do instant funding accounts have profit targets or drawdown rules?

Yes, most instant funding accounts still have profit targets and drawdown limits, even though they skip the evaluation phase. As our review confirms, instant funding accounts implement rules such as drawdowns to manage trader risk.

Can new traders use instant funding accounts?

New traders can apply, but strict rules and instant access to capital often favor those with experience and discipline. Instant funding works best for traders with risk management experience already in place.

How fast can I withdraw profits from an instant funding account?

Most platforms allow withdrawals within 7 to 14 days, but policies vary by firm. Withdrawal periods for instant funding accounts typically range from 7 to 14 days depending on the firm’s specific terms.

Are instant funding accounts more expensive than challenge accounts?

They usually cost more upfront because you skip the evaluation stage for immediate capital access. Instant funding carries higher fees than challenge-based models in most cases.

Recommended

- Instant Funding Prop Firms 2026: Are They Worth It? (2026) | Responsible Trading

- Instant Funding Programs vs. Brokers: Which is Better for You? (2026) | Responsible Trading

- Funded Account Trading Strategies That Actually Work in 2026 (2026) | Responsible Trading

- Instant Funding Programs vs. Evaluation Programs: Which is Better for You? (2026) | Responsible Trading

- Demo trading accounts: Your risk-free path to smarter trading

- How To Scale A Trading Account FAST In 2025 (Proven System) | FxShop24 Marketplace